By Arthur S. Guarino

A debt ceiling crisis is an extremely real possibility if Congress does not pass the necessary legislation in time. The financial and economic consequences of such inaction will affect global currency markets, stock markets, and the United States’ economy in a serious way.

The more things change, the more they stay the same. This old adage remains true now as the federal government is severely running low on money and the nation’s debt ceiling must be raised so that the first outright default in United States’ history is avoided. The Congressional Budget Office (CBO) projects that in October the Treasury Department will not be able to acquire funds since the debt ceiling will be reached and further borrowing is not possible without Congressional authorization. This last occurred in November 2015 when the debt limit was suspended at $18.1 trillion. The debt ceiling was increased, but another raise is necessary or else the nation will not be able to pay its obligations and possibly set off financial fireworks that will affect holders of Treasury instruments to Social Security recipients, not to mention a government shutdown. How the United States arrived at this point is the first step in understanding the dilemma.

What is the Debt Ceiling?

In essence, the debt ceiling is the amount of money that the United States can legally owe. Both houses of Congress must vote on establishing the debt ceiling which is “a limit to pay for obligations already incurred,” according to a Government Accounting Office (GAO) Report in February 2011. The Treasury Department explains the debt ceiling as the “total amount that the United States government is authorized to borrow to meet its existing legal obligations, including Social Security and Medicare benefits, military salaries, interest on the national debt, tax refunds, and other payments. . . It simply allows the government to finance existing legal obligations that Congresses and presidents of both parties have made in the past.” This explanation is very broad but also very true since the debt ceiling allows the federal government to continue operations on many diverse levels and parties that are owed money can rest assured they will be paid.

Once the borrowing limit is reached, the Treasury then operates under “extraordinary measures” so that government spending and obligations are financed temporarily until that ceiling is raised again by Congress. Currently, the debt ceiling is at $19.8 trillion when a new limit was established on March 16th, 2017. But that amount will most likely be surpassed in October 2017. And it is very possible that the eventual new debt ceiling that is reached will surpass the nation’s Gross Domestic Product (GDP).

The debt ceiling was enacted by Congress in 1917 in order to placate fiscal conservatives who worried about excessive spending due to the nation entering World War I. The debt ceiling has been raised numerous times. In fact, since 1960 Congress acted on 78 separate occasions to raise the debt ceiling. And now it is happening again. According to Harry Stein, director of Fiscal Policy at the Center for American Progress, “Essentially, the debt ceiling is like getting a credit card bill. You’ve made the decisions, those have consequences for the debt, and now you have to raise the debt ceiling in order to accommodate the laws that you’ve already passed.”

Congress has increased the dollar amount on the debt ceiling over the years so that the federal government does not default. Congress has raised the debt ceiling ten times in the last decade and four times each in the years 2008 and 2009. The problem is that the debt ceiling has gone through controversy when the Congress and the president cannot find common ground on fiscal policy. Most recently this happened in 2013 when Congress threatened not to increase the debt limit in order to curtail spending in the 2013 Fiscal Year budget. But, generally, debt ceiling increases have occurred with and without controversy.

While Congress has seen it necessary to raise the debt ceiling over the years, the amount has been reflective of the federal government’s spending. For example, in 1996, the debt ceiling was $5.5 trillion but from 1997 to 2001 it was $5.95 trillion. In 2002, it was increased to $6.4 trillion and from 2003 to 2004 it was $7.384 trillion. But every year from 2004 to 2017 it has increased and despite the expected confrontation between Congress and the president, it will most likely go up again.

| Year | Debt Ceiling Amount (in trillions) |

|---|---|

| 1996 | $5.500 |

| 1997 to 2001 | $5.950 |

| 2002 | $6.400 |

| 2003 to 2004 | $7.384 |

| 2005 | $8.184 |

| 2006 | $8.965 |

| 2007 | $9.815 |

| 2008 | $10.615 |

| 2009 | $12.104 |

| 2010 | $14.294 |

| 2011 | $15.194 |

| 2012 | $16.394 |

| 2013 | $16.699 |

| 2015 | $18.113 |

| 2017 | $19.800 |

Consequences of Not Raising the Debt Ceiling

The current controversy is whether Congress will raise the debt ceiling as Treasury Secretary Steve Mnuchin hopes they will. However, if Congress does not raise the debt ceiling, then there could be serious financial and economic consequences for the United States starting with the value of the dollar on world markets. If the debt ceiling is not raised, then foreign exchange markets will see a dangerous decline in the dollar’s value since investors will sell their dollars and instead purchase euros, yens, or Swiss francs. Investors will want certainty in their holdings as opposed to the uncertainty of when and by how much the debt ceiling will be raised. While a lower dollar will mean American companies will be able to sell more of their products overseas, it will also mean that interest rates will increase. The dollar could see a severe run as investors head toward safe havens in the currency markets.

Making matters worse is that as investors dump dollars in favor of safe and reliable alternatives, the potential for inflation will rise exponentially. The world markets will be flooded with dollars and inflation will rise to levels not seen since the 1970’s. Investors just want a good rate of return and certainty and they have a number of alternative investments. By dumping dollars, the market will be inundated and American consumers will see prices rise. The question then is how soon will such a spike in inflation occur and how long will it last? A side effect will also be that the dollar will lose its reputation as a safe haven and there will probably be calls by different nations to end the dollar’s unique role as the world’s reserve currency.

If no deal can be reached on the debt ceiling, then the nation’s credit rating will most likely drop. In the summer of 2011 Congress and President Obama had a long and fierce debt limit battle which moved Standard and Poor’s to downgrade the credit rating of the United States from AAA to AA+. This will cause interest rates to increase on Treasury instruments since investor’s premiums will rise. As the rule in finance goes: As bond ratings go down, interest rates go up. In 2012, the GAO reported that delays in increasing the debt ceiling in 2011 cost American taxpayers an estimated $1.3 billion for the Fiscal Year.

If no debt ceiling deal is reached then the stock markets will see a 10 to 15%, even 20% drop. The markets do not like bad news and lack of a deal on the debt ceiling will throw the markets for a loop. Stock investors will go liquid by holding cash or go into money market instruments as they wait for certainty between Congress and the president. There is precedent for this scenario: the Dow Jones Industrial Average lost approximately 2,000 points in the lead up to and the aftermath of the 2011 debt ceiling debate in a matter of days. In fact, the Dow fell 635 points on August 8th, 2011 in one of the worst single-day drops in the market’s history the day following Standard and Poor’s downgrade. Investors will not only go liquid but rush into gold causing it to really spike.

Another serious consequence of not raising the debt ceiling, is the loss of faith in Congress and the Trump Administration by Americans and investors around the world. If Congress cannot get together and decide on a proper debt ceiling increase, this will cause Americans to not only lose faith in its political leaders but probably be the catalyst for a house cleaning in the 2018 elections. Americans want to see long-awaited action and cooperation in Congress on something and a deal on the debt ceiling could be the turning point. But if the House and Senate cannot arrive at a deal, then there could be big changes in next year’s midterm elections. Even within the Trump Administration, there is disagreement. Trump wants a debt ceiling deal tied in with spending for the border wall with Mexico, while Treasury Secretary Mnuchin is calling for a “clean,” no strings attached debt ceiling raise not involving any spending cuts or new projects. However, Budget Director Mick Mulvaney wants to attach some type of overhauled spending plan to the debt ceiling increase. Critics charge that the Trump Administration is not speaking with one voice which further confuses the situation. If no deal is reached, there will most likely be a government shutdown. Whether it will exceed the previous shutdowns in the Clinton and Obama terms remains to be seen. But a government shutdown will be the least of the problems in the failure to reach a debt ceiling agreement.

Possible Financial Crisis

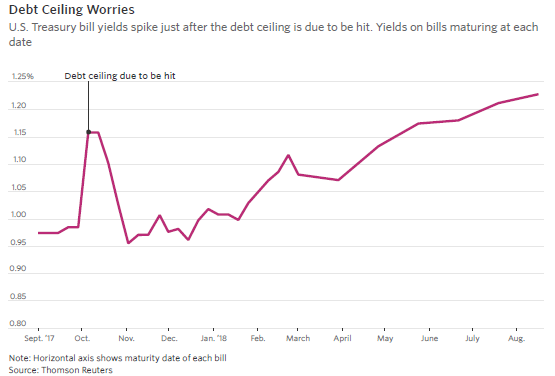

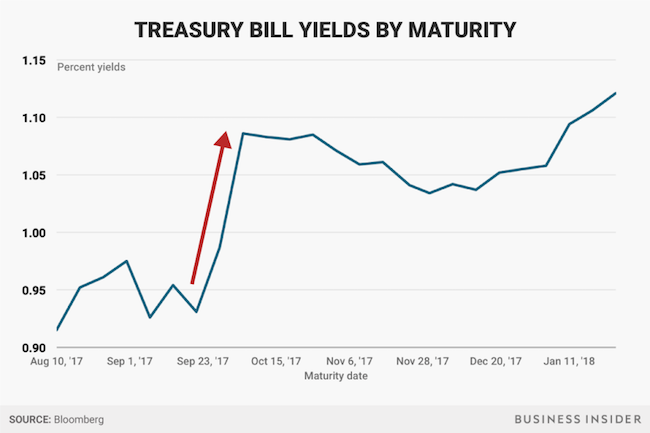

The biggest concern among economists, financial analysts, and policymakers is that there is a high possibility of a financial crisis if no deal is worked out. The Treasury Department is calling for a debt ceiling increase by September 29th so that the federal government can pay its debts, interest, short-term obligations, and expenses. However, if nothing occurs by then, the potential for a run on the dollar, a stock market crash, a serious spike in interest rates, or panic in global financial markets are real possibilities. The effect of no debt ceiling deal is already being felt as bond traders are increasing the yields on short-term Treasury instruments. This could be the first wave of more reaction to come from the financial markets.