Can Green bonds work?

Green bonds are seen by many environmentalists and socially responsible investors as a way to help the world’s ecological well-being and also achieve a good return on investment. But like any investment vehicle it has its good points and risks. The question is whether green bonds are financially viable?

By Professor Arthur S. Guarino

As more individuals invest in order to achieve a better return, there are those who wish to also help the environment. Some investment analysts and portfolio managers feel that achieving a return that beats the major indices as well as inflation over the long run is mutually exclusive from socially responsible investing. But a growing trend occurring on a global basis is the use of eco-friendly financial instruments or otherwise known as green bonds. Globally, investors, corporations, municipalities, nations, and major investment houses are assembling green bonds designed to finance projects benefiting cities, states, and communities with eco-friendly projects such as waste water treatment plants, energy efficient projects, and clean transport vehicles such as busses. While green bonds are still in their infancy, they are growing in popularity and are even regarded as financially viable by return conscious investors.

What are Green Bonds?

Green bonds are generally defined as debt obligations in which the proceeds are used to finance projects beneficial to the natural environment. More specifically, the International Capital Markets Association (ICMA) has published the Green Bond Principles describing green bonds as “any type of bond instrument where the proceeds will be exclusively applied to finance or re-finance, in part or in full, new and/or existing eligible Green Projects.” The Green Bond Principles are designed to promote disclosure and transparency, while encouraging integrity in order to facilitate the growth of the issuance of green bonds. These are primarily appealing to investors ranging from institutions such as mutual funds to pensions to individuals who want socially responsible investments in their portfolios that are eco-friendly and offer a fixed rate of return in the form of annuity payments or interest. Green bonds can be used for financing new projects and re-financing existing projects. Green bonds are used to finance new industries or provide financial capital for unique and innovative answers to old dilemmas affecting the environment.

The real goal of green bonds is to use a relatively conservative investment vehicle – fixed-income financial instruments providing an income stream to investors for periods of 20, 25, 30 or possibly 50 years – to finance projects benefiting the environment. This can include projects such as providing clean water for a metropolitan area, promoting solar or wind projects that are regarded as renewable energy sources, or by companies such as LG Chem Limited of South Korea that issued green bonds in 2019 to finance eco-friendly projects such as renewable energy and electric vehicles worth US $1.56 billion.

Green bonds work like any other type of bond in which the cash flow from the project would be used to pay the interest and later the principle on the instrument. The project cash flows could come from the revenues of the project such as fees for a water waste treatment plant or taxes collected from the town, city, or state as in a general obligation bond. Bonds, overall, are considered the most relatively safest investment since they depend on a project’s cash flow in order to pay the fixed interest over an extended time period. But to be deemed a green bond, it must be used to finance or re-finance an environmentally friendly project. Green bonds can also have tax incentives such as tax-free interest for the investor and tax credits.

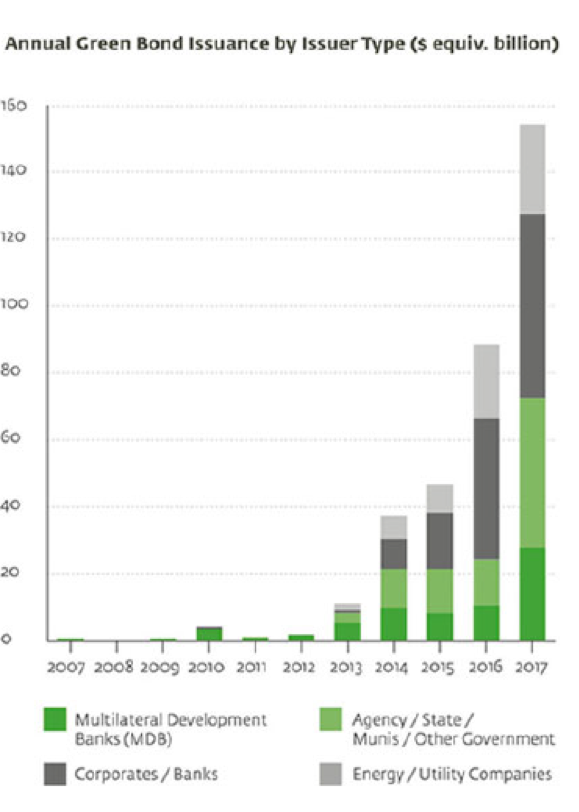

The first green bond ever formulated occurred in 2007 by the European Investment Bank when it issued a Climate Awareness Bond for €600 million. Since then there have been hundreds of green bonds issued by financial institutions such as JP Morgan, Blackrock, Zurich Insurance Group, Natixis, HSBC, and Bank of America Merrill Lynch. The International Finance Corporation (IFC) has issued more than $7 billion of green bonds since 2010 to private investors in which the proceeds have been used for projects such as wind power in Panama and solar power in Mozambique. The green bond market has grown substantially: in 2012, only $2.6 billion in green bonds were issued but in 2017 there was $161 billion issued globally. The green bond market still has a way to grow since these bonds are only a bit more than 1 percent of the $53 trillion global bond market.

Under the Green Bond Principles, the projects that have been recognized as “green” or eco-friendly include:

- Renewable energy

- Energy efficiency

- Pollution control and control

- Environmentally sustainable management of living natural resources and land use

- Terrestrial and aquatic biodiversity conservation

- Clean transportation

- Sustainable water management

- Climate change adaptation

- Eco-efficient and/or circular economy adapted products, production technologies and processes

- Green buildings meeting regional, national or internationally recognized standards or certifications

Positive aspects of Green Bonds

Green bonds have a number of positive aspects for both investors and issuers.

First, there have been growing interest in green bonds since they offer investors who are environmentally conscious new and different opportunities in their portfolios. These growing opportunities not only helps an investor in terms of diversification in their portfolios, but also make an impact with funding projects that have benefits to the global environment. There are increasing numbers of socially responsible investors who are looking to invest not just for the sake of getting a better return, but also to help the environment through financing projects that will assist in reaching this objective. This is evident by information from the Climate Bonds Initiative (CBI) which reported that the number of new green bonds issued in 2018 increased to US$163.7 billion, which rose 3 percent from 2017. These growing opportunities mean that issuers have increased the number of bonds available to the buying public. For example, Fuzhou-based Industrial Bank was the second largest green bond issuer after Fannie Mae in the United States, collecting a combined US$29.7 billion in funds in 2018.

Secondly, along with these growing opportunities has come further diversity in the types of green bonds being issued. For example, there are sovereign green bonds which are issued by the national, central government of a country. Sovereign green bonds are denominated in local currency or possibly in foreign currency. This can work as other sovereign bonds do and offer investors a chance to take advantage of different currency valuations while funding a project beneficial to the nation’s environment. Sovereign green bonds have been issued by the government of the Netherlands in May 2019 for €6 billion for a variety of climate friendly projects such as clean transportation, climate change adaptation, and renewable energy. In 2017, Nigeria became the first African nation issuing a sovereign green bond in which proceeds were allocated for projects promoting the switch to a low-emission economy along with climate resilient growth.

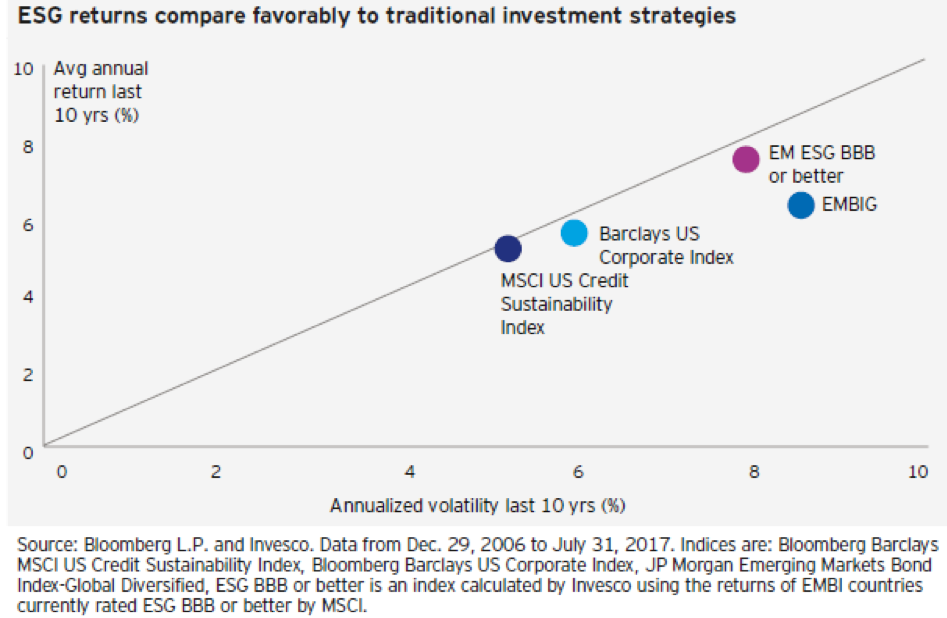

A third benefit is that many green bonds were found by Moody’s to be quality or investment grade. That is, green bonds have lower chance of failure or defaulting even if they have a lower interest rate than non-investment grade bonds. Moody’s found that 97 percent of green bonds were investment grade quality while 43 percent had AAA rating or the best bond rating possible. Moody’s research found that green bonds had a return of 1.7 percent for the first quarter of 2016 versus 2.5 percent return for the Bank of America Merrill Lynch Global Bond Index. While the return on green bonds may not match those of general bond indices, it can be noted that investment grade bonds allow investors to sleep soundly at night.

Finally, green bonds help advance green projects. For example, the state of New Mexico in the southwest United States issued their first green bonds in early 2019 and the instruments were certified by the CBI. The bonds will fund a new eco-friendly waste water system for the city of Santa Fe. The investors for the bond offering made bids totaling US$52 million for a US$13.5 million issue. The bonds have a maturity of 20 years and were issued when interest rates are relatively low. More municipalities in the United States are taking definite action in the move toward green bonds. In California, state officials moved in 2018 toward taking steps in combating climate change by signing the Green Bond Pledge creating a bond market in order to finance environmentally friendly and carbon-free projects designed to help the state’s infrastructure. Hopefully, these green bonds will help California close the US$400 billion funding gap it faces in the next decade for needed infrastructure projects that will improve the state.

Risks associated with Green Bonds

Like any other investment, green bonds hold certain types of risk that concern investors and issuers.

First, individual investors who have small holdings may have a difficult time purchasing green bonds. The controversy regarding the availability of green bonds is that institutional investors, such as mutual funds, pensions, or insurance companies, have been known to purchase large blocks of these instruments. This will cause small investors to be discouraged in purchasing green bonds. Until more green bonds are issued in smaller lots, it may be very difficult for socially responsible small investors to purchase eco-friendly investments.

Secondly, meeting the requirements for a green bond may be deemed as too daunting for an issuer. Potential issuers, such as a municipality or a state, may find it very difficult to meet the requirements set forth in the Green Bond Principles. The issuers may deem it too costly and very difficult given the additional reporting requirements for a green bond.

Thirdly, the definition of a green bond may vary from country to country and city to city. For example, China permits green bonds in order to finance clean coal projects while rules in the West do not. Some countries may seek to find loopholes in the Green Bond Principles or even try to bend the rules to their advantage. This may mislead investors and could actually hurt the bond’s value in the long run. CBI rejected US$24.5 billion of green bonds in 2018 which did not meet its requirements.

Fourth, research has shown that green bonds may be too expensive to issue. According to a study by David Larcker and Edward Watts at Stanford University Graduate School of Business in California on average investment banks charged approximately 10 percent in order to sponsor green bond offerings. The reason is that green bonds are regarded as relatively more difficult to market. This will cause the issuer to pay higher fees than for a normal bond issuance.

Fifth, it is possible that a country, state, or municipality may issue too much debt including green bonds. Debt can be beneficial in being able to finance a much-needed eco-friendly infrastructure project. But the problem could arise that the entity has gone into too much debt and cannot make its promised interest payments. Also, if the project cannot pay for itself then the bond may suffer severe cash flow problems. Either way, this will affect the green bond’s quality and even hurt the chances of more green bonds being issued in the future.

What does the future hold for Green Bonds?

There is nothing wrong with green bonds as an investment alternative. The market for socially responsible investments is growing and many analysts deem them a viable and credible alternative. Green bonds are really in their infancy and it may take some years until there are enough to satisfy demand. Until then, investors must have patience till the marketplace has enough supply.