The global economy is facing an unprecedented crisis threatening everyone. With the spread of Covid 19, governments in various cities, states, and nations have shut down numerous businesses and forced millions to either work from home (if they can do so) or become furloughed or terminated them from their jobs. Those who have been furloughed or fired, are without work and neither the workers nor their employers know exactly when they will be able to return. This involves workers in restaurants, retail stores, manufacturing plants, and service companies. The fear of policymakers and healthcare leaders is that workers will contract the Covid 19 virus and spread it to their co-workers, families, friends, and customers. This will cause more people to need hospitalization, extensive medical care, or die in a relatively short time period. The other problem is that consumers have stopped spending and will no longer go to bars, restaurants, or retail stores until the pandemic subsides.

The laid off workers in the United States have filed for unemployment benefits. But the problem is that many of the states are unequipped to handle the millions of people filing for unemployment benefits in such a short time period. Their systems are either antiquated for a vast number of unemployment benefit applicants or that meeting the requirements to receive benefits has become much more difficult than in the past. This has resulted in laid off workers relying on meager savings that will evaporate in a matter of days. According to a survey taken in 2019, 69% of respondents stated that they have under $1,000 in a savings account versus 58% in 2018. It gets worse: The top reason respondents gave for not saving more was due to the fact that they were living paycheck to paycheck. This is a very scary economic and financial situation and it has taken a pandemic to bring it to the forefront.

Presently, there has been a call for the introduction of universal basic income, or UBI, as a way to deal with the present financial crisis. UBI has been used in various nations and even in the United States. UBI would be used in addition to unemployment benefits since it would be administered and given by the Federal government of the United States to each individual who has been furloughed or laid off. UBI has been criticized as a handout and a disincentive to seek employment, full or part time, or even to work ever again. But as things stand currently, policymakers and economists may have no other choice in order to prevent people from starving or being thrown out of their homes.

What is UBI?

UBI, also known as guaranteed basic income (GBI), allows every individual, irrespective if they are employed or not, to receive a monthly income that is enough to provide them a living above the poverty line. UBI is designed to be given to every individual regardless of their own personal economic situation. It does not matter what their net worth is or their level of income on a yearly, quarterly or monthly basis and no means testing is used.

UBI does not have basic requirement standards for receiving an income that needs to be satisfied. In this case, there are no requirements that must be fulfilled such as voting, satisfying military duty, attending school or taking classes, or any type of community service. UBI is a set amount of money provided by the state or federal government which must be sufficient to meet daily living requirements and will be provided regardless of a person’s race, age, social level, gender, or economic background.

The amount that can be awarded to an individual would been to be determined by the Federal government. Some have stated it should be $1,000 while others argue the amount should be $2,000 per month. But whatever the amount, the premise of no strings attached would remain the same. But regardless of the amount that would be allocated for each person, there are important reasons for using UBI.

First among the reasons for UBI is that it can be used as a buffer against the systematic problems existing within the macroeconomy. UBI could be a potential policy tool to offset economic problems within society such as poverty, income disparities, and stagnating wage and income growth. Prior to the financial crisis brought about by Covid 19, wages were either growing at a slow rate or were stagnant. With wages not keeping up with the cost of living and many households needing two or more earners just to keep their heads above water, UBI could act as the income supplement many desperately need. As things now stand, it is not unusual for both husband and wife to work in order to make ends meet. Prior to the Covid 19 crisis when the unemployment rate was low, many Americans did not feel confident about their job future or their financial situation, whether in the long or short-term. To make matters worse, millions of Americans are deep in debt due to home mortgages, auto loans, student loans, and credit cards. Even if one spouse suffered job loss, this could spell serious financial consequences for any household.

Another key reason for UBI is the potential it has to assist those workers employed in dead-end or low paying jobs. UBI could help workers employed by fast food restaurants, landscapers, aides in nursing homes, or at a car wash. These workers make minimum wage and have minimal or no benefits and UBI could act as a greatly needed financial supplement. Individuals working in these jobs put in fifty to sixty hours on a weekly basis and do not earn enough to cover their living expenses such as food, rent, or health insurance. These workers have a difficult time providing for a family and are caught in a perpetual cycle of poverty becoming the working poor. UBI could provide additional income that could possibly bridge the wage gap these workers experience daily and give them some breathing room. It should be kept in mind that many of these workers are not usually union members and their opportunity of making a decent wage or even the possibility of a living wage are slim or none.

Lastly, UBI could be a less costly substitute for social welfare programs as presently administered. UBI does not have the paternalism of social welfare programs, benefit requirements to remain eligible in such plans, nor the costly bureaucracy often associated with such governmental entities. UBI would eliminate the social stigma of such assistance programs. The benefit would also involve a higher degree of government efficiency and a lower cost of program administration.

Current economic crisis

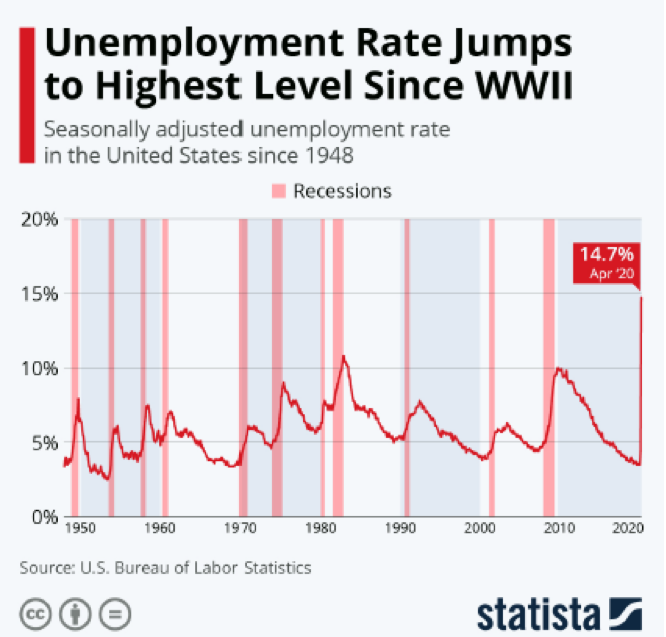

The macroeconomy of the United States is in freefall. Within a matter of seven weeks over 33 million workers have lost their jobs and more layoffs are expected for the fall of 2020. With very few exceptions, just about every industry is laying off workers and will continue to do so until the end of 2020.

The airline industry has been hit especially hard since social distancing has become the norm for many people. Among the casualties are Virgin Atlantic which announced cutting 3,150 jobs on May 5th as well as retiring its iconic Boeing 747-700 planes a year early. United Airlines Holdings, Incorporated recently announced that it plans to cut approximately 30% of its white-collar workers starting in October. European airlines are not immune to the industry downfall as British Airways stated that it has no expectations of returning to its passenger numbers of 2019 and therefore will reduce its workforce by 12,000 this year. Air Canada announced in March that it was laying off 5,100, or 50%, of its flight crews while Scandinavian Airlinessaid it would temporarily let go of 10,000 employees, or 90% of staff. Every airline has been hit badly and no one really knows how many will survive this crisis without government assistance.

But if the airline industry is being hit by a devastating blow, then ancillary industries are also feeling the effects. Pebblebrook Hotel Trust, the owner of over 50 hotels in the United States, laid off 50% of its employees, or 4,000 workers on March 17. The company’s chief executive officer, Jon Bortz, informed the Los Angeles Times that it may need to lay off an additional 2,000 employees very soon. On April 12th, a union representing workers at Walt Disney World said the company will furlough 43,000 employees starting mid-April. While the theme parks have been closed since March 16th, only 200 essential workers will remain in order to maintain them. In late April, TripAdvisor, the online travel company, announced layoffs exceeding 900 employees equaling 25% of its workforce.

If airlines are not flying and cutting back service and employees, it also means they will not purchase jet planes. This has hurt other companies related to the airline industry such as Boeing and General Electric. In early April, Boeing, one of the largest exporters of the United States, announced a plan offering voluntary layoff to its employees as a cost cutting measure since orders for its planes have been slashed dramatically. Boeing’s biggest rival, Airbus SE, has also cut back on production. General Electric, which manufactures jet engines for Boeing and Airbus, has reduced its workforce by 25% in that division.

Switching fields, the automobile industry will suffer major losses due to severely reduced sales, lower capital expenditures, supply chain disruptions, increased macroeconomic uncertainty, and health concerns for its workers. Companies such as Ford Motor and General Motors have suspended their quarterly dividend payments and have faced operational interruptions that have led to severe financial losses and deep questions about their futures. Will Ford Motor Company be forced into bankruptcy while General Motors may face the threat of bankruptcy for the second time in little more than a decade? With Ford and General Motors suffering financial losses, what will this mean for their vendors and suppliers? If Ford and General Motors suffer financial collapse, then there will be a domino effect throughout the Midwestern part of the United States as their vendors and suppliers will also experience either bankruptcy or be forced to permanently close their operations. This will result in thousands of layoffs and cause the unemployment numbers in the United States to reach unprecedented levels.

Besides the effect the economic crisis will have on diverse industries, there is also the strong possibility of deflation rearing its ugly head in the global economy. On May 12th, the United States Labor Department reported that consumer prices fell 0.8% in April versus the numbers reported for March. The problem here is that the Consumer Price Index has increased only 0.3% from that of April 2019. There was a decline in core prices, which excludes food and energy prices, of 0.4% which accounted for the steepest decline in its history. The decline in consumer prices in April marked the second consecutive month that consumer prices have dropped since the start of the Covid 19 pandemic in the United States and the largest drop since 2008. Whether this is a long or short-term deflationary movement is still too early to call, but a decline in consumer prices will be a clear sign that the American economy is headed for a long, perilous dive.

UBI is needed now

Regardless of where Covid 19 started, its financial and economic impact has been devastating. The modern-day food line in the United States has been miles of cars waiting two to three hours for a bag or two of groceries. Families have been forced to reduce their spending for items such as clothing, entertainment, and even food. In order to try to lessen the financial blow that many are suffering, a supplemental source of income is necessary. This is where UBI could come in to help families put food on the table and give them a source of hope until the macroeconomy begins to improve. Now no one can really tell when that will happen. But until then, UBI could cushion the economic and financial blow many are feeling.

The short-term problem with UBI is where the funds will come from. The Federal government will either need to borrow $2 to $3 trillion per month to provide money for monthly benefits for American workers or run the printing presses on a non-stop basis. But with interest rates as low as they are, borrowing may be the best alternative at the present moment. If that is not enough, then printing money by the Federal government will need to substantially increase. There will be critics who will argue that the danger of hyperinflation will ruin the United States. But the danger of an economic depression is at the doorstep of not only the United States, but every other developed country. Desperate times call for desperate measures. And desperate times also calls for outside-the-box thinking.