Joe Biden has won the brutal contest against Donald Trump for the nation’s highest political office. The presidential campaign was unique since it was completed under the shadow of the Covid-19 pandemic. Covid-19 did not cast one ballot but it was an influential factor in the contest and will still play a key role in the nation’s economic health. Because of Covid-19, many financial and economic decisions will be based on how to combat the deadly spread of the disease while reviving the nation’s macroeconomy.

Even so, President-elect Joe Biden must face three key challenges affecting the nation’s macro-economy. These challenges include jobs, growth of the economy in the form of the gross domestic product (GDP), and trade. If Biden can slow the spread of Covid-19 while also reducing the number of hospitalizations and deaths nationwide and bringing back jobs, increasing the nation’s GDP, and solving trade differences with China and Europe, and accomplishing this all in four years, then his chances of re-election are certainly assured. But this is not an easy task, and will require all of his intelligence and acumen, as well as the best talent he can immediately assemble.

Jobs, Jobs, Jobs

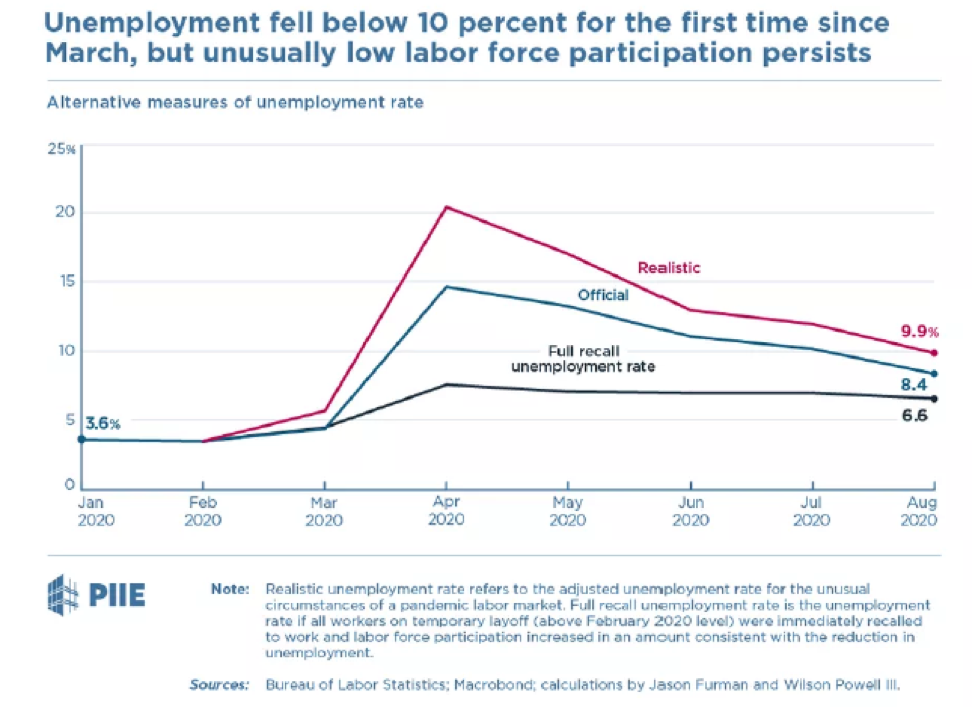

The situation regarding jobs in the United States is dire. The American economy is consumer based which means that spending keeps it going. But in order for consumers to spend, they must have jobs. However, due to the slowing American economy, jobs have been decreasing and key data does not point to in a positive direction. According to the Department of Labor, for the week ending December 19th, the seasonally adjusted number of jobless claims totaled 803,000 which was a decrease from the previous week of 892,000 claims. For the 4-week moving average there were 814,250 claims filed for unemployment benefits.

The figures only get worse as the total number of continued weeks claimed for unemployment benefits in all programs for the week ending December 5th came to 20,363,675. If one were to examine the claims filed for unemployment benefits in all programs for the same week in December 2019, that amount came to 1,757,802 in weekly unemployment figures. This is an incredible jump in the period of one year. What makes matters worse is the for the week ending December 5th, there were 24 states that had Extended Benefits which means that unemployed individuals who had exhausted their initial unemployment benefits could file for additional funds that could possibly last another six months, if the states had that much money available. Among the states providing Extended Benefits are California, New York, New Jersey, Ohio, and Texas, to name a few.

While these figures are quite frightening for economists and policymakers, long-term prospects for an economic recovery appear very dim. According to economics professor Betsey Stevenson from the University of Michigan, “If we don’t get all the workers back, we can never have a V-shaped recovery. Everybody should be worried about making sure that we don’t leave workers behind.” A V-shaped recovery refers to a fairly immediate and sustained rebound in the macroeconomy after it has suffered a sharp and rapid decline.

If jobs do not eventually start to come back, workers will become discouraged and there will be a severe and probably permanent decline in the country’s labor force participation rate. The problem is that workers of different skills, ages, talents, and educational training will become severely discouraged from looking for jobs of any type or retire earlier than they had anticipated. This could cause the labor market to tighten up and possibly have wages increase in order to entice workers to return to work. But the problem also is that many of these workers who are now out of the labor force will cut back on their spending and actually reduce the size of the American economy.

There are certain industries that are seeing significant drops in employment. These include brick-and-mortar stores, food services, health care, hotels, bars, pubs, and restaurants. If the coronavirus spreads at a greater rate than earlier in 2020, and a dark winter becomes reality in 2021, then the number of unemployed across the United States will only increase at a rate that could surpass previous estimates. President-elect Biden must work with the House of Representatives and the Senate in order to create jobs programs similar to what occurred with President Franklin Roosevelt from 1933 to 1936. This would mean passing legislation that creating jobs by fixing the nation’s infrastructure, providing aid to restaurants, bars, and pubs, and expanding job training programs in every state.

The Congress must provide a minimum of $2 trillion in aid to small and midsize businesses that should be in the form of low-interest loans that would have an extended maturity period. Just giving grants to businesses would seem like a handout that small and midsize firms would be ashamed in taking. But loans aimed specifically at allowing small and midsized businesses to hire people could possibly provide more jobs and help the American economy recover sooner than anticipated.

Raise GDP

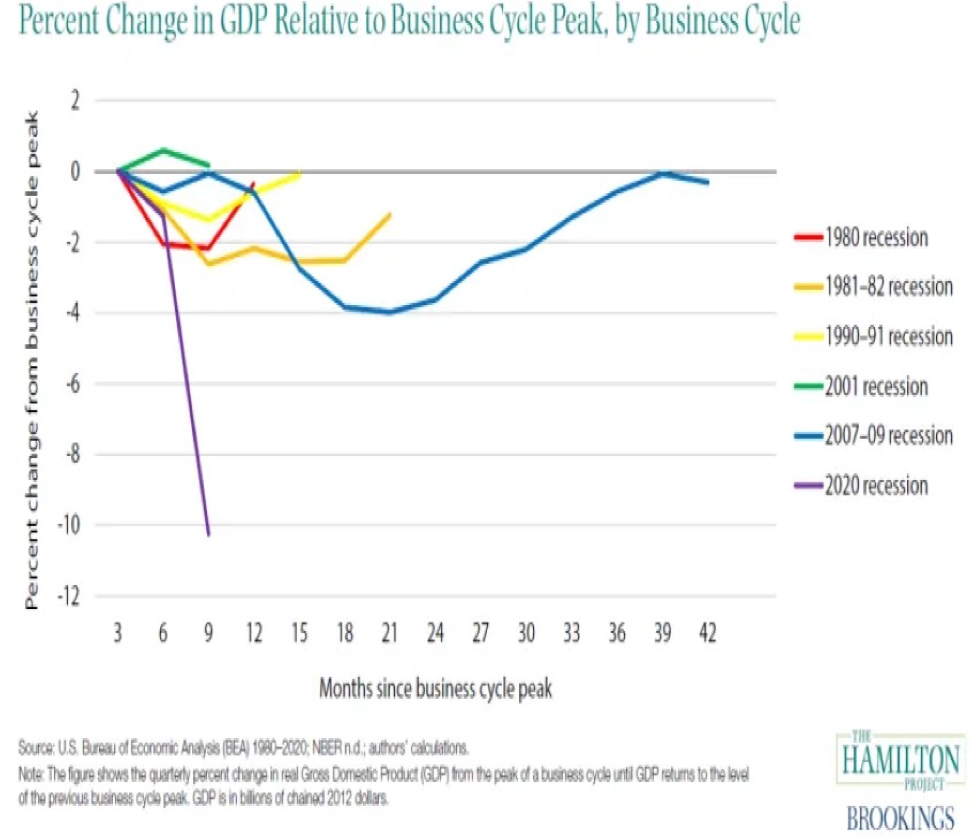

Economic growth in any macroeconomy is generally measured by the improvement in a nation’s GDP. Due to the pandemic, the GDP of the United States has taken a dramatic hit and trying to get it back to its previous level will be very difficult for the Biden Administration. According to the Bureau of Economic Analysis (BEA), from the end of 2019, the American economy had two consecutive quarters of economic decline in GDP that was so bad that it saw the severest record-setting quarterly drop of economic output of 9.1 percent in the second quarter of 2020. This drop signaled the end of 128 consecutive months of economic expansion which was the longest in the history of the United States. What makes this even worse is that GDP on a quarterly basis has never seen a decline that exceeded 3 percent since such economic records were started to be kept in 1947. The problem is that with such a sudden, severe, and sharp decline in the American economy, Biden will have a very difficult time in trying to achieve pre-pandemic levels in economic growth.

The nation’s industrial production has been seriously hurt by the severe slowdown in which aspects such as manufacturing output, mining, and utility production have seen drastic downturns starting in March 2020. This has affected almost 13 million workers in the nation’s industrial sector. If the nation’s economy slows down further, companies in the industrial sector will lay off millions of workers and seek increased use of automation in order to reduce costs and maintain or even increase production.

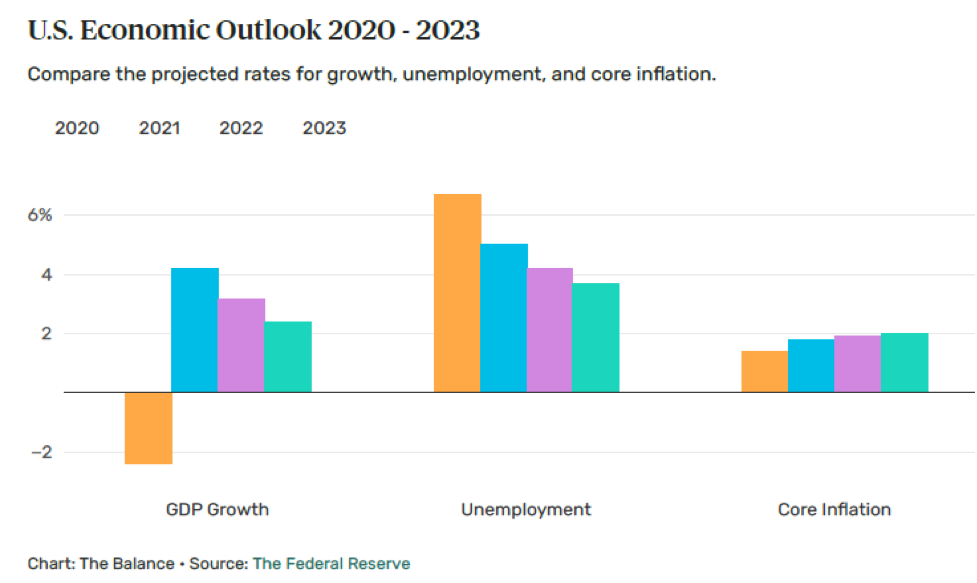

It is not just the American economy that is facing a drastic slowdown, but also the rest of the world. The research organization, RAND Europe has estimated that the world’s economy is seeing a loss in output at a rate of $3.4 trillion on an annual basis. With the best-case scenario of a vaccine being distributed in record time to the rest of the world, RAND Europe estimates that the loss in global industrial output would only decline to $1.2 trillion, or approximately $103 billion every month. The Federal Open Market Committee of the Federal Reserve Bank has recently forecasted that U.S. GDP growth will be expected to shrink by 2.4 percent in 2020 but will see a rise in 2021 of 4.2 percent. The problem here is that the rate of growth could slow even further in subsequent years if all does not go according to plan.

There are two key areas that the Biden Administration must improve in order to boost the nation’s GDP: Consumer spending and Business investment.

Consumer spending has seen a dramatic drop in 2020, even though it has shown signs of recovering. Among the areas that have been hurt badly are restaurants with numerous closing either temporarily or permanently, airlines with flights almost empty or, at best, one-quarter full, and service companies with only a modicum of customers showing up. Reports show that consumer spending on services saw a reduction of 10.2 percent in the first quarter in 2020 while spending at restaurants and hotels came down approximately 30 percent on an annual basis. The American auto industry has suffered serious damage due to consumers cutting back on buying or leasing new vehicles in which spending in that sector dropped precipitously by a rate of 33.2 percent. One of the few sectors that was able to weather the drop in spending due to the pandemic and the forced shutdowns it caused were companies that provide groceries since Americans stocked up at an amazing rate. Spending on such items as groceries fell only 1.3 percent as a result of the pandemic. Probably the best way to increase consumer spending is an increase in jobs: When people are employed, they are more likely to spend thereby creating more jobs for restaurant workers, airline workers, and service employees.

Business investment is vital since it means that companies must purchase new equipment, materials, or technologies in order to expand or grow their operations. Due to the pandemic, only certain sectors saw growth in business investment. For example, there was a 5 percent increase in businesses acquiring information processing equipment even though GDP fell in the second quarter in 2020. Businesses must make investments that will improve productivity as well as efficiency in their operations rather than just on safety equipment or supplies. Improving safety is important, but will it also increase output and subsequently revenues and net profits? The forecast for 2020 is that real fixed business investment will decrease 4.9 percent, while real inventory investment will fall $64.9 billion at the same time and affecting corporate profits before tax by showing a drop of 9.6 percent. The Biden Administration must do what it can to stimulate business investment that will help companies grow in the long-run whether by low-to-no interest loans, grants, or tax credits.

Increase trade

Trade plays a key role in the American macroeconomy and President-elect Biden will need to deal with various factors immediately after assuming office. To begin with, Biden will make an effort to reverse Trump’s policy of “America first” and “America alone” when it comes to trade and other international situations. Biden will more than likely work with other nations in formulating policy that will deal with trade, climate change, and the Covid-19 pandemic. The odds are good that Biden will be supporting a rules-based system when it comes to trade but make sure that it is fair and a level playing field for all participants. Biden will be concerned with returning jobs to the United States whether it is in the service sector or manufacturing which was part of his presidential campaign strategy of “build back better.” Biden knows that jobs play a key role in building the American economy or else he will not be re-elected in 2024. Biden stated during his 2020 campaign to “use the full power of the federal government to rebuild U.S. domestic manufacturing capacity of our supply chains for critical products.”

Another concern will be the situation with China. The Chinese have been building their economy in an aggressive manner and regions such as the European Union have become wary of what the future holds. President-elect Biden recognizes the challenge the United States faces with China and he will probably take a different tactic than his predecessor. This will mean working with other nations in order to create a fair and competitive trade policy rather than trying to have the United States go it alone. This will not be easy, since Trump has alienated many allies and have them doubting whether they can trust the United States anymore. Biden knows that the trade relationship with China is necessary for American farmers and manufacturers who want to sell their goods and products in a rapidly expanding economy that is eager for quality. The problem is that Biden must try to reopen the trade door with China that Trump deemed a national security threat. Biden knows that a key first step to creating a new and better trade relationship with China would be to end tariffs on $370 billion of imports from China that the Trump administration imposed in these past four years. These tariffs have actually become a tax that American consumers must pay on goods and products imported from China and that the Chinese have reciprocated by imposing tariffs on American farm products such as soy and corn. Biden knows it will not be easy to re-establish a good trade relationship with China, but it must be done.

Finally, Biden must contend with trying to get the United States into trade agreements that the Trump administration slammed the door in a loud and forceful manner. Nations such as China, Australia, South Korea, and Japan are part of the Regional Comprehensive Economic Partnership (RCEP) which acts as a response to the Trans Pacific Partnership (TPP). Trump stated that the TPP would hurt the American worker and the macroeconomy. However, the response was the RCEP that includes approximately one-third of the globe’s GDP and does not need to worry about the trade deal that the United States, Canada, and Mexico were able to forge in Trump’s time in office. Biden must do what he can to get the United States into the Comprehensive and Progressive Agreement for the TPP or else face ridicule from those supporting free trade and the potential for more jobs in the United States. Biden must be able to work with nations in order to strike trade deals with regions who are looking to exchange products with the United States after the debacle by the Trump administration when it came to trade or lack of it.

Biden’s full plate

President-elect Joe Biden has a very full plate when it comes to dealing with the American economy and he knows it. The Covid-19 pandemic has made things very dangerous and the possibility of the American economy slipping further into a deep hole is all too real. Biden must do what he can to increase the number of jobs, but it means getting back into trade deals that will be fair and help expand the American economy. Getting the American economy back on its feet will not be easy, nor occur overnight. But Biden must work at a very fast speed because 2024 will be here before we know it.