Can wealth taxes solve economic inequality?

The uneven distribution of wealth is regarded as an economic problem that may have serious societal ramifications. The concern among economists and financial analysts is whether a wealth tax will level the playing field between socioeconomic classes.

For a number of years in the United States, a severe disparity has evolved between the wealthy, middle class, and poor. Many economists and policymakers state that the wealthy are only accumulating more wealth, while the poor are growing in number, and the middle class is shrinking. Statistics and studies have shown that more wealth in terms of financial and capital assets seems to be concentrated in the hands of the wealthy as well as higher amounts of income whether in the form of interest, dividends, or capital gains. The problem is that less assets, whether in the form of money or other economic resources, is being held by those who could truly use it and need it to survive or improve their station in life.

A growing cry in the United States is to have a wealth tax that could help redistribute financial and economic assets to those who truly need it. Critics claim a wealth tax could level the economic playing field and redistribute wealth in a more equitable manner. But others counter this argument by stating that the redistribution of wealth would actually do more harm than good to the economic growth of the United States in the long run. While both sides make persuasive arguments for and against a wealth tax, the key objective is to create a viable and fair solution to the economic and financial inequality that is rampant in the United States today.

Wealth inequality in the United States

At present, the situation in the United States regarding wealth inequality is more disparate than perhaps any other time in its history. Just by examining the numbers, one can see that a shift has occurred in the past forty years in which the rich are getting richer and the poor are increasing in number. The transformation could be seen as starting in the early 1980’s when changes in the nation’s federal tax law saw a shift that favored the country’s wealthy in which billionaires actually paid 79 percent less in taxes as a measured share of their wealth.

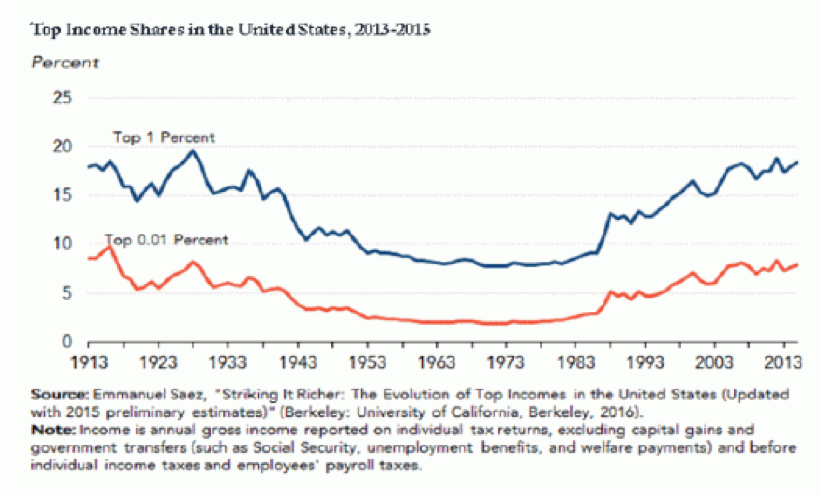

Things only improved for the wealthiest as the nation’s top 0.1 percent which consists of households having wealth exceeding $100 million, saw their tax payments as a percentage of their wealth decrease by approximately 73 percent. With the Reagan Revolution of the early 1980’s, the wealthy saw their tax liability drop substantially so that their level of wealth actually started to grow better than they ever saw previously. The wealthy since then have only increased their level of holdings and financial wellbeing in which the share that the nation’s wealthiest, at the top 0.01 percent, hold has increased significantly from 2.3 percent in 1980 to 9.6 percent in 2018. This same group has also seen their income, in the same time period, go from 1.5 percent to 4.6 percent. Current estimates state that the top 1 percent of the American population hold almost 20 percent of the nation’s income while the top 0.01 percent have approximately 8 percent.

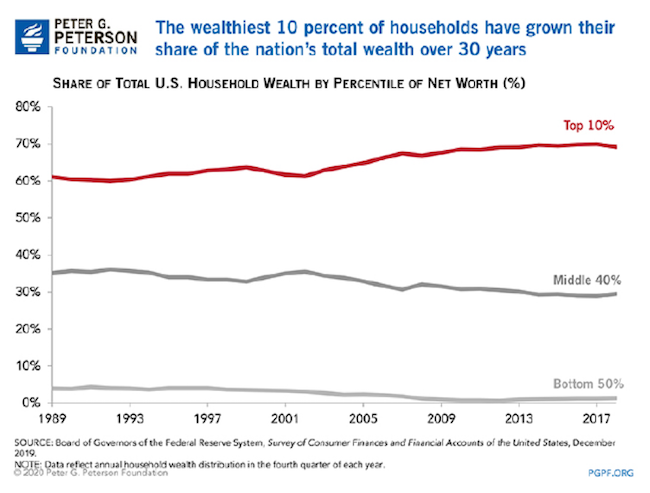

As a result, an exorbitant amount of wealth has been accumulated by those in industry, especially high-tech entrepreneurs. These include Jeff Bezos at Amazon.com at over $109 billion, Bill Gates at Microsoft at $107 billion, Mark Zuckerberg at Facebook at $72 billion, and Elon Musk at Tesla at $24 billion. The Congressional Budget Office (CBO) has reported that the top 10 percent of families in the United States have more than 75 percent of all accumulated wealth in the nation.

Studies have shown that the situation regarding wealth inequality is only getting worse. University of California, Berkeley Professors Emmanuel Saez and Gabriel Zucman have estimated that the share of wealth that the 0.01 percent hold has almost tripled to exceed 20 percent since the late 1970s. But, the share of wealth held by the bottom 90 percent of the American population has decreased from 35 percent to 25 percent.

If a longer-term view were examined, the statistics are even more dramatic. In 1962, the top 1 percent and bottom 90 percent each had approximately 35 percent of the nation’s wealth. Then the disparity only grew starting in the 1980’s to the point where in 2016 the top 1 percent saw their share of wealth climb to 39 percent while the bottom 90 percent witnessed their allocation go down to 20 percent. The CBO has reported that inflation-adjusted after-tax earnings of the top 1 percent of wealthiest Americans grew by 275 percent in the years from 1979 to 2007. For the bottom 20 percent of wage earners in the United States after-tax earnings grew at only 18 percent.

Perhaps a good statistical measure of wealth inequality and lopsided income distribution in the United States today is the Gini Coefficient. Developed by the Italian statistician and sociologist Corrado Gini, the model attempts to show how the disparity has grown over the last few decades. The Gini Coefficient has shown that the closer the coefficient is to one, then the closer its income distribution is to absolute inequality. For the United States, the Gini Coefficient was below 40 percent in 1964 and actually saw a slight decline throughout the 1970s. But starting in 1981, the Gini Coefficient started to rise and continued its movement upward to the point where the CIA Factbook had it at 45 percent. In sum, wealth inequality and income distribution, from a statistical perspective has only gotten worse.

The situation can best be characterized by Yale economics professor, Robert Shiller, who stated that, “The most important problem that we are facing now today, I think, is rising inequality in the United States and elsewhere in the world.”

How a wealth tax works

A wealth tax has been argued as a method to not only redistribute wealth in a society but also to address the controversy of wealth inequality. The first step in assessing a wealth tax is that the tax would be on the net wealth or net worth of an individual. Here the total amount of assets, or items of value that a person owns must be assessed as to how much each is worth. This could include the value of each home a person owns, the financial assets they may have, perhaps expensive works of art, or companies that are owned outright. Next, the amount of liabilities or debts would be calculated. That is, the mortgages and loans an individual must pay back with interest over time. The total assets minus the total liabilities equals a person’s net worth or net wealth.

Once the net wealth is calculated, then there could be a tax on that amount. There are several proposals as to how much the tax would be. Some proposals state a flat tax of 5 percent or even 10 percent on a person’s net wealth. Other proposals want to tax the amount over $10 million of the individual’s net wealth. Still other ideas state that any amount above $1 billion in net wealth should be taxed.

Other proposals to the wealth tax state that certain items could be exempt from the net wealth calculation. For example, a certain number of common stocks a person holds, or interest in a business employing a certain number of workers. There is also the proposal of a uniform exemption in which amounts below a threshold would not be taxed. Senator Elizabeth Warren, a democrat from Massachusetts, puts forth the proposal that only families whose wealth exceeds $50 million would be taxed and the rate would start at 2 percent on their holdings. And at this level the top 1 percent of income earners would be liable for 97 percent of the tax. Senator Bernie Sanders, independent representing the state of Vermont, has proposed a wealth tax that places rates of up to 8 percent annually on wealth exceeding $10 billion.

Other proposals would be for low and progressive rates. The argument for a low tax rate would be so a wealth tax could be imposed annually on individuals who meet the criteria for taxation. A low rate would aim to keep the growth of wealth at high levels in check and be able to spread funds to a greater segment of the rest of society on a more frequent basis. Progressive rates would call for higher marginal tax rates for very high wealth levels.

The premise for a wealth tax as opposed to an income tax is that there are ways to shelter income from taxation. A classic example would be interest from municipal bonds in which the interest is free from federal, state, and city tax. The more an individual invests in municipal bonds, the greater the amount that would be sheltered from income taxes. Under a wealth tax, the value of the municipal bonds would be included as part the net wealth calculation and would ultimately be taxed. An individual would not be able to enjoy any sheltering of income from taxation here. Another example would be investing in growth stocks. A wealthy individual could also invest heavily in growth stocks that usually do not pay dividends for a number of years. This would help an individual avoid taxation on dividends as income. But that person could not avoid a wealth tax since the value of those growth stocks would be part of the calculation for a wealth tax. The key idea is that a wealth tax would not only tax the wealthy while creating a level playing field in society, but also make it more difficult to avoid taxation through loopholes.

Controversy surrounding wealth tax

The concept of a wealth tax is not without its share of controversy. A key aspect of the controversy is that a wealth tax could possibly affect the macroeconomy of the United States. Critics have charged that a wealth tax would be a disincentive for the accumulation of wealth through investments in risky assets and projects. It has long been held that the American economy has seen its growth due to investors placing their money in assets, inventions, and projects that have a certain degree of risk. A wealth tax would dissuade these investors from making investments in the next Microsoft or Apple since, if they were very successful, they would be penalized by a wealth tax. The general idea has been that investors want to invest in the next Apple or Microsoft since the potential reward would be substantial in the long run. This acts as a key motivating factor to not only invest in a new venture, but also take on risks they normally would not. Critics feel a wealth tax does not reward innovation nor does it motivate an investor to take risks that could lead to potentially large rewards. Critics argue that in the long run this would also hurt the economic growth, investment, productivity, and savings of the United States.

The wealth tax is not a law in the United States. In order to become a federal tax law, it would need to go through the U.S. Congress and that would probably be a messy situation. But if the law went through Congress, there would be numerous lobbying groups that would try every way they could to put loopholes into the law. This would mean removing the effectiveness of the law by placing loopholes that would probably favor having a third home that would be exempt from the definition of wealth under the law. Or that growth stocks would be exempt from being part of the wealth calculation. Lobbying groups would do everything they could to remove the efficacy of the wealth tax and lower its potential to level the playing field regarding wealth in the United States.

Another controversy regarding the wealth tax is how to properly value assets and when. The problem here is that assets would have to be valued at a particular point in time and using a certain valuation method. That is for certain assets, would depreciation need to be included in the asset’s valuation and what method should be used. For assets such as works of art, how and when should they be valued and by whom? How should homes be valued? What and who should value antiques, collectibles, and precious metals? How should a privately-held company be valued? For publicly traded financial assets, such as common stocks or corporate bonds, valuation can be accomplished in a relatively easy manner. But for others, it will be difficult.

“The thing to remember is that really wealthy people don’t hold all their assets in easy-to-value areas like stock and bonds,” states John Koskinen, former commissioner of the IRS. “A lot of them have artwork that’s worth a lot of money. A lot of them have investments in privately held corporations or in investment vehicles that do not give regular valuations.” The Internal Revenue Service would need to outfit itself in order to deal with the wealth tax valuations so that no one will be able to evade the regulation. The problem also exists of individuals doing their best to either evade paying the tax altogether or making donations to museums or giving the assets to family, friends, or charities in order to lessen their tax bite.

Finally, critics of the wealth tax feel it would be a violation of the “takings clause” of the Fifth Amendment. The Amendment states that private property shall not be taken for public use without just compensation. A wealth tax could be challenged in federal court as a violation of the takings clause since property is being unjustly and illegally taking and that there is class warfare on the wealthy. Whether a wealth tax would hold up in federal court or judged to be constitutional if it reached the United States Supreme Court is anybody’s guess. But there surely are individuals who would do all they could to contest the legitimacy of the law since it was their assets that would be taxed.

Is a wealth tax possible?

The controversy at present is the change in wealth and income in the United States that many feel is slanted significantly toward the wealthy. At one time, there was more balance in the American economy in which the opportunity to acquire wealth was a distinct possibility for all and the chance to move up the socioeconomic ladder was realistic. But today, many feel that unless a person is born of the correct skin color, in the right zip code, or the correct family lineage, then the chances of moving up are slim or none. In many cases, not even a college education may be the opportunity to escape poverty and move into the middle class or upper class. Proponents of a wealth tax feel it would be the best way to make society a level playing field and give others a chance they would normally not have.