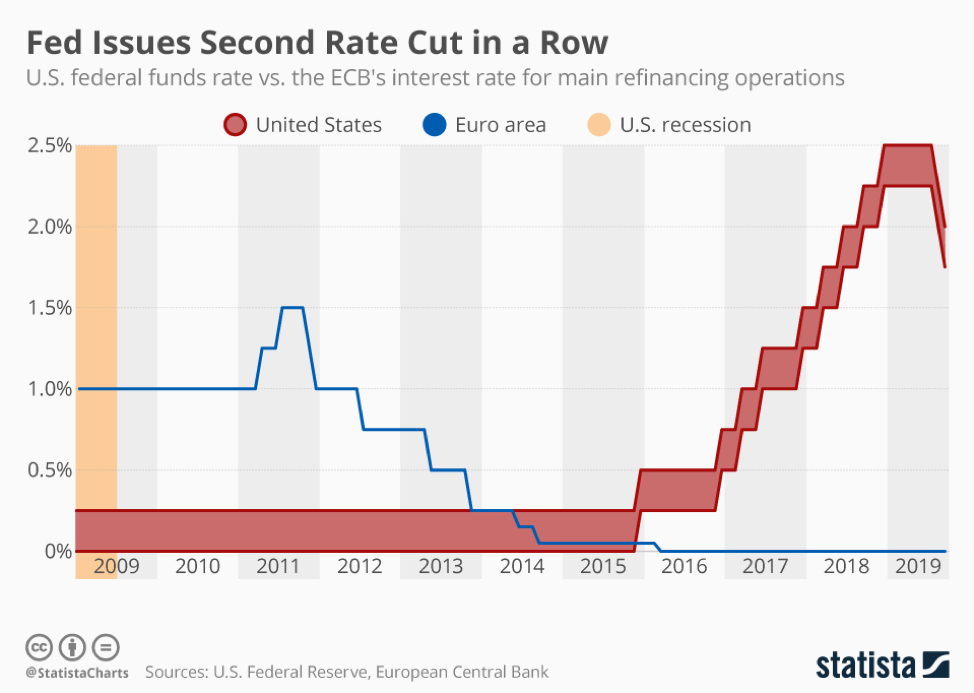

The Federal Reserve Bank announced on Wednesday that it was dropping its benchmark interest rate by a quarter percent for the second time in two months due to the concern of a slowing macro-economy. But even with a rate cut of this type, President Trump was not happy with the move and called for rates to drop to zero percent and even into negative territory. Trump even went so far as to attack Fed Chair Jerome Powell in a series of Tweets by stating that “Jay Powell and the Federal Reserve Fail Again.” Trump attacked Chairman Powell by stating that the Fed’s announcement showed “No ‘guts,’ no sense, no vision! A terrible communicator!” These malicious attacks are really an absolute sign that Donald Trump is making nonsensical attacks on Fed monetary policy that is trying to stave off a recession in the United States and keep some wiggle room if the worst-case scenario were to occur.

Reasons for the Fed’s actions

Jerome Powell is very worried about the current and future state of the American economy. First, there is the trade war between the United States and China, started by the Trump Administration. Powell realizes that tariffs imposed by the United States on goods imported from China are having an effect on American farmers, manufacturers, and consumers. American farmers are having a difficult time selling their agricultural products on the Chinese market due to reciprocal tariffs imposed by the Chinese government. American farmers are seeing their revenues decline, farm bankruptcy’s increase, and having a difficult time selling in competitive world markets. Manufacturers are also having rough time selling their goods in China due to tariffs and a slowdown in the global economy. American consumers are starting to see the price of Chinese-made goods increase in price forcing them to either pay more or not buy at all. The situation will only worsen since the Trump Administration plans to place tariffs on almost all goods imported from China by the end of 2019 and could be on top of the tariffs on $360 billion worth of Chinese-made products.

Secondly, the Fed is also concerned about the slowing global economy. The Chinese economy is seeing its macro-economy slow down to a growth rate in the single digits. Germany is staring at the very real possibility of a recession, while the financial and economic implications of Brexit are still unknown for both Britain and the European Union. Globally, manufacturing is slowing down which will ultimately affect the American economy.

Thirdly, the Fed is also worried about the low inflation rate in the United States. With inflation at 1.6 percent, the Fed is concerned that this may actually be a strong sign of a slowing economy. The Fed would like to see inflation at is target rate of 2 percent. But that economic goal has been hard to achieve. If inflation were a manageable 2 percent or even 3 percent, then it could be a sign that the American economy is showing signs of economic growth. But if a recession were to hit the American economy, inflation could go lower and the danger of deflation could only compound a dangerous situation. Based on these concerns, Jerome Powell has a plate full of problems that he must deal with.

What Trump wants

Donald Trump has called for zero interest rates for some time in order to stave off the financial problems the rest of the world is encountering. By having zero interest rates, he feels firms and consumers can still borrow at no cost and keep making purchases. Because the United States is a consumer-based economy, Trump wants individuals to keep purchasing goods, products, and services with borrowed money at no cost. However, even if interest rates drop to zero percent there will be a lag time before American consumers see it in their credit card rates. There is often language in credit card agreements permitting card issuers to charge the highest prime rate in use during the preceding 60-day time period. Even if there is a .25 percent rate cut on a credit card balance of $10,000 this would only reduce the minimum card payment by $2 per month. This will not be sufficient to incentivize consumers to use their credit cards to spend and therefore boost the American economy.

Trump also feels that zero rates would mean that the Federal government could issue new debt for longer maturities at no cost. The idea here is that the tax cut plan passed in 2017, the Tax Cust and Job Act, would pay for itself and possibly reduce the Federal budget deficit. But the problem with this thinking is that bond investors may want a higher premium on U.S. Treasuries, such as bonds and notes, due to future uncertainty and therefore raise long-term Treasury yields even more. This could lower the rating on Treasury instruments and cause uncertainty in the bond markets, global and domestic. Treasury debt is regarded by investors as the safest in the world since they can rely on the fact that the United States has never reneged on its debt nor missed an interest payment. Also, Treasury instruments are not callable which adds to their attractiveness to investors. The Treasury Department could not call in old bonds and notes and refinance them with zero interest instruments.

But Trump is also calling for Treasury bonds to have an extended maturity to 50 years. As Trump stated in a recent tweet: “The Federal Reserve should get our interest rates down to ZERO, or less, and we should then start to refinance our debt. . . INTEREST COST COULD BE BROUGHT WAY DOWN, while at the same time substantially lengthening the term.” The key question is whether the bonds markets would react favorably to an ultralong maturity for U.S. debt that pays zero interest. By holding such debt, bond investors may call for a high-risk premium for holding such an instrument. And the problem is that Treasury instruments do not carry such a risk premium.

Trump also wants zero interest rates in order to help companies and farmers affected by the trade war with China. With zero interest rates, American companies affected by tariffs on Chinese-made goods would have one less cost to worry about and possibly not pass on the cost to their customers. Whether this could work in the long-run is a huge gamble by the Trump Administration since the length of the trade war with China is uncertain.

But Trump also wants negative interest rates. Jerome Powell has stated that he is not in favor of negative interest rates. The problem is that in a situation with debt issued using negative interest rates, the lender must pay the borrower for the borrower’s use of the principal. This may cause bond investors to stay away from Treasury instruments if they were to use negative interest rates. Then the big question is where the Federal government will get its money to keep operating.

Why lower interest rates could be a danger

Lower interest could be a danger for several reasons. First, there are parties who would be hurt since they rely on financial instruments such as bonds and certificates of deposit (CDs) for their income. This includes senior citizens, pension funds, mutual funds, and annuities that need the interest income from such instruments. Senior citizens have limited sources of income and their risk tolerance is very low thus prohibiting them from venturing into stocks, whether common or preferred. But with zero interest rates pension funds will have an extremely difficult time making payments to pensioners and will need to seek other financial instruments that may carry more risk than they can incur. There are mutual funds that have a stated objective of income and this comes in the form of interest and/or dividends. If the interest portion disappears, then the current yield on the mutual fund could make a serious drop and hurt the investors of those portfolios. The same could be said of annuities since investors purchase them for the steady stream of income over an extended time period.

Another group that would be hurt by zero interest rates are savers. There are individuals outside of senior citizens who are habitual savers putting away money for that proverbial rainy day, a child’s education fund, or just for the sake of saving. With zero interest rates, these savers are being punished since their money will not be keeping up with the rate of inflation even if it is as low currently. There are savers who are risk averse and will not or cannot put their money into the stock market where they could purchase common or preferred stock that pays high dividends. These savers exist and are being punished for saving for the long-term.

Another group that will get hurt financially will be those affected by negative interest rates. Generally, lenders who purchase CDs need the interest income they generate. And these lenders are often senior citizens in their 70’s, 80’s, 90’s. The problem is trying to explain to them that money will actually be taken from their account rather than receiving interest as they are accustomed to. Making this change to losing money on their CDs would be a real shock and very difficult to comprehend. For so long they are used to receiving interest when they put their money in a bank CD and now, they will actually incur a cost for doing so.

Be careful what you wish for. . .

Donald Trump wants lower, zero, or negative interest rates to spur on the American economy. But he should be concerned that seeking lower interest rates would be a sign to the financial markets that there may be a recession in the short-term. Yet the Fed knows that lower interest rates is a key tool for reviving the American economy in case of a recession, no matter how bad this economic downturn would be. If rates are extremely low, then the Feed may need to start a new round of Quantitative Easing and dramatically inflate its balance sheet as it did during the Financial Crisis of 2008-2009. Even then, the effects were not immediately felt after a few initial rounds of Quantitative Easing. Lower interest rates, zero rates, or negative rates also may not be the answer to stave off an economic recession and would hurt savers in the meantime.