The implications of the 1% stock buyback excise tax

Stock buybacks have faced criticism, but now will be taxed for the first time. What will this mean for investors and public corporations?

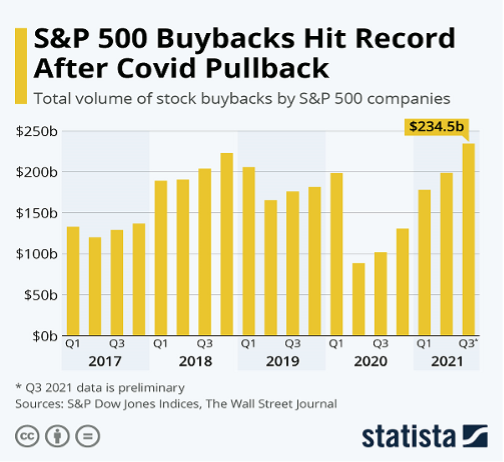

For many years, stock buybacks have been used by publicly traded corporations as a method to return cash to shareholders while also increasing the value of its common stock. The practice has come under criticism in recent years from those who regard it as a tax dodge. But others feel that it is the prerogative of the issuing corporation of what they wish to do with the company’s excess cash while also rewarding investors for the risk they have taken.

Recently, the Inflation Reduction Act of 2022 was passed in the United States House of Representatives and the Senate in which a major provision of the law is a 1 percent excise tax on the net dollar amount of the common stock that has been repurchased. Companies such as Apple, Colgate Palmolive, Alphabet, Microsoft, Bank of America, and others will be affected in their proposed plans to repurchase, or buy back, shares of their common stock from shareholders. Proponents of the legislation feel it is about time in order to allow equity in how cash is distributed to investors. Opponents feel this legislation is just a “nuisance tax” that will hurt the stock markets, issuing corporations, and shareholders. Either way, this excise tax is the first time such an action has been taken on an investing incentive of Corporate America that has long been deemed as an untouchable perk of stock ownership.

What are stock buybacks?

Simply put, a stock buyback, or a stock repurchase, happens when a corporation buys back its own common stock from its shareholders. A company may have an excess of cash and wishes to distribute some of these funds to its shareholders by buying back their own shares of common stock. Here a company owns its shares again resulting in a reduction of shares outstanding in the marketplace. One way a company can perform a stock buyback is by going into the open market and become like any other purchaser of its stock. Another way a company can buy back its shares is through a tender offer.

In a tender offer, shareholders are presented with an offer or opportunity by the company to submit, or tender, some or all of their shares within a certain time period. The tender offer must state the number of shares the company is willing to buy back as well as the price it will pay for the shares, usually at a premium or above the market price. If the shareholders accept the offer, they must state the number of shares they will tender and the price they will accept. When the company gets all the offers, it must determine the correct amount to purchase the shares at the lowest cost.

When a company repurchases its own shares, it can retire them and designate them as treasury stock or shares to be held in the company’s treasury department. These treasury shares no longer pay dividends and may be reissued at some point in the future if the company needs an infusion of cash for a merger or acquisition or to purchase an asset and sell shares of the treasury stock in order to do so.

Stock buybacks were not always permitted legally since they were considered as a way to manipulate a stock’s market price by artificially boosting it. However, in 1982, Rule 10b-18 was issued by the Securities and Exchange Commission which provided a legal process allowing stock buybacks. A key stipulation of the rule is that the corporation buying back its shares is not allowed to repurchase more than 25 percent of the average daily volume of shares.

The case for stock buybacks

There are various reasons why a corporation has stock buybacks:

Raise market price of undervalued shares: There are times when a company’s executive management team feels that their common stock price is lower than it should be or undervalued. Management may feel that the stock market has not given the stock its due by having a higher market price. Management may arrive at the conclusion that the best way to remedy this perceived injustice is to repurchase its common shares and cause the stock price to attain the level where it really should be. Management could also be under pressure from the company’s board of directors or its shareholders that the stock market price is too low and that it should be raised 10, 15, or 20 percent. Management may be pressured to raise the market price or else face being replaced by another group of managers who can successfully perform the task.

Maximize shareholder wealth by distributing cash: There are times when shareholders or the board of directors feel that the company is holding too much cash in its coffers. Cash is the most liquid of assets a company holds but will usually earn the lowest return on assets (ROA). Shareholders may feel that the excess cash should be distributed to them as a return or reward for investing in the company instead of remaining in the company’s vault. Management may feel that given industry standards or possibly planning for an acquisition or have funds in case of an emergency, a substantial amount of cash is important. Many activist investors have recently pushed management teams to increase the number of stock buybacks so they can have quick access to cash for a short-term investment in the company. The key is that shareholders will not just receive the market price or a tender offer, but the stock buyback will include a premium for buying back the shares. This will cause management to pay out more cash than they could be ready to give.

Raise a company’s earnings per share (EPS): A management team may feel pressured by the board of directors that the company’s EPS is too low and therefore not an attractive investment for potential shareholders. Wall Street stock analysts often cite EPS as a key reason for purchasing the stock and tout companies that have a consistently rising EPS, whether it is a growth company or a mature firm. For many companies this is very difficult to perform given the ups and downs of the macroeconomy, the industry the company is in, and unknown events that could lurk around the corner. When a company buys back their common shares outstanding, but the company’s net profits or earnings stay the same, the company’s EPS will increase quarterly and annually. This will many times be perceived as a highly favorable event by the company’s shareholders, stock analysts, and Wall Street and ultimately result in a higher stock market price.

Cash outflow reduction: When a company buys back its own shares, this will decrease the dividends it must pay. On a cash flow statement, the dividends paid to shareholders, whether to common stock or preferred stockholders, is regarded as a drain on cash. Analysts will see this and often make a negative report on the company’s financial situation, which will drive down the market price. If there are fewer shares outstanding due to a stock buyback, fewer cash dividends will be paid and more cash will be retained by the company. Analysts will pick up on this move by management and sing high praises for the action, thereby raising the market price of the stock. Healthy cash flow for any company is always a positive aspect that management should strive for, but through a stock buyback it may be done in order to appease only stock analysts. An example of this is the stock buyback announced by chipmaker Broadcom in April 2018 in which they stated that they would buy back approximately $12 billion worth of their common shares. Tom Krause, the Chief Financial Officer of Broadcom stated that the company was “maintaining our policy of delivering 50 percent of trailing 12-month free cash flow to shareholders in the form of dividends while adding the ability to use the balance of our free cash flow not only for acquisitions but also for opportunistic buybacks.”

Reduce dilution of shares outstanding: Many corporations have generous employee stock option plans (ESOPs) which are designed to reward mid-level and upper-level managers for their performance in running their departments. Sometimes ESOPs are used in place of monetary bonuses. However, an excessive number of shares awarded in ESOPs will have the problem of diluting the number of outstanding shares when the options are exercised by the managers. This could eventually cause the company’s stock price to drop when the options are exercised. A stock buyback could be used to offset the increase of shares outstanding in an ESOP and keep the stock price high or what management perceives at a favorable level.

How the excise tax works

The Inflation Reduction Act of 2022 was signed into law on August 16th containing the provision of a non-deductible 1 percent excise tax on certain types of stock buybacks. The key aspect of the legislation is that there will be an excise tax equaling 1 percent of the fair market value of any shares of common stock a publicly traded domestic corporation buys back or repurchases during its fiscal year. The corporation, to be eligible for the excise tax, must have its common stock traded on an established securities market, such as the NYSE or NASDAQ, and that it has repurchases exceeding $1 million as per the aggregate tax year. These qualifying corporations also include non-U.S. stock markets meeting the regulatory requirements of the Securities Exchange Act of 1934. Qualifying markets includes the London Stock Exchange as well as the Tokyo Stock Exchange. The tax will be placed on the value of whatever share being repurchased unless the buyback is being taxed as a dividend.

The effective date of the excise tax will apply to shares being repurchased after December 31, 2022. Also, included under the excise tax will be those domestic subsidiaries purchasing the common stock of their non-U.S. corporate parents as long as the shares are being traded on a regulated and established securities exchange. The excise tax would affect publicly traded companies not individual shareholders.

The key aspect to know about the excise tax is that it is reduced by the value of any stock that the corporation issues during the same fiscal year which can include any compensatory stock. A financial example of how the excise tax would work is the following: if a corporation repurchases $100 million of common stock in its fiscal year but issues other stock for cash or compensation reasons in that same year for $10 million then the 1 percent excise tax base amount would be $90 million. ($100 million − $10 million = $90 million) This means the excise tax would actually be $900,000. ($90 million X 1% = $900,000)

There are exclusions to the excise tax which include:

- Where a repurchase is treated as a dividend for U.S. federal income tax purposes

- If there is a repurchase by a regulated investment company or a real estate investment trust (REIT)

- Where a repurchase by a securities dealer is performed in the ordinary course of business

- A repurchase that is part of certain types of tax-free and tax-deferred reorganization transactions where neither a gain nor a loss is recognized by the shareholder

There are other exclusions listed the legislation that public corporations must be aware of and whether they apply to their own situations.

What the excise tax means for corporations

Publicly traded corporations that have extensively used stock buybacks are now faced with a dilemma. They must now decide whether the 1 percent excise tax is worth the financial pain or that they should change their buyback strategy. Companies such as Alphabet, Amazon.com, and Meta must ask themselves if they should continue to pay cash to their shareholders via a stock buyback or start paying dividends. That is, these are companies that do not pay dividends and feel the best way to distribute cash to shareholders is via a stock buyback.

There are other companies, such as Colgate-Palmolive, who pay both dividends and have stock buybacks. These companies must determine whether they can continue to do both or resort to increasing their dividend payouts. These companies must perform a cost-benefit analysis as well as re-evaluate their dividend policy. They must determine how important it is to keep their shareholders happy or else risk possible activist rebellions.

For some, stock buybacks do not have a great reputation. Senator Charles Schumer of New York has flatly stated, “I hate stock buybacks. . . I think they’re one of the most self-serving things that Corporate America does instead of investing in workers and in training and in research and in equipment.” Individuals from this side of the argument feel that cash could be better spent in other ways in a corporation. This group welcomes this unprecedented legislation affecting corporate strategy.

On the other side, opponents of the excise tax feel that it will hurt companies in how they want to allocate their cash. The U.S. Chamber of Commerce opposes the legislation on the grounds that it “would distort the efficient movement of capital to where it can be put to best use and will diminish the value of Americans’ retirement savings.”

Arguments have been made by both sides, but now that the excise tax is reality, many publicly traded corporations must make decisions on what to do with their cash that will be the most efficient and effective.