Activist investors: More harm than good

By Arthur Guarino

The role of activist investors in American boardrooms has grown in recent years. But the dilemma is whether they make a positive impact on a company or do more harm than good.

American business schools have long taught the financial concept of “shareholder wealth maximization” but in the past decade activist investors have taken the idea to an entirely new level. In many cases, management teams of many corporations have earnestly tried their best to maximize shareholder wealth, but many activist investors feel there have been missed opportunities resulting in misspent capital and poor returns. But even if activist investors have focused on achieving better returns, their intentions may actually cause more harm than good for other investors, the firm itself, and even the American economy in the long term.

What are activist investors?

Activist investors usually purchase a minority stock position in a publicly traded company with the idea of introducing strategies to increase profits, cut costs, and overall improve operating performance under their guidance, wisdom, and experience. They seek to work with the firm’s management team by introducing new techniques that will ultimately maximize long and short-term value for all shareholders and run the firm more efficiently and effectively.

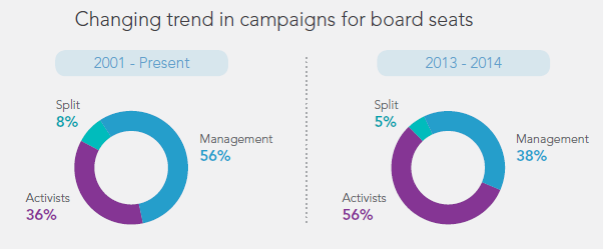

Activist investors often purchase common voting shares in the target company that will be enough so they can possibly have a seat on the board of directors. Activist investors usually take their ideas directly to senior management, and often the board, advocating immediate change. The problem occurs when management rejects or refuses to work with activist investors since they may not have sufficient knowledge or experience in that particular industry or about the company itself.

This may spur the activist investor to possibly purchase a larger position in the firm’s ownership and thereby place their people on the board. Another activist investor’s tactic is to obtain support of pension funds and institutional investors who can pressure the board and management as large shareholders so that change can occur. These investors are often hedge funds who must disclose their activist share by filing a Schedule 13D with the U.S. Securities and Exchange Commission (SEC). This regulation must be followed when an investment surpasses 5 percent of the company’s voting common stock. The problem is what the possible harmful outcomes may be to the firm and other shareholders.

Problems caused by Activist Investors

While activist investors see themselves as the salvation of an underperforming company and helping fellow shareholders achieve greater wealth than they ever imagined from their holdings, they can actually be making things worse.

There is the situation with Nelson Peltz and his hedge fund, Trian Fund, and their investment in DuPont. Peltz, through Trian, purchased shares in DuPont and demanded that it cut costs by $4 billion or else take full control of the chemical giant without input from management. DuPont relented and significantly reduced costs including globally laying off 5,000 people in 2016 or 10 percent of its workforce. DuPont was also forced to make huge cuts in its research and development areas, thereby hurting its competitive edge as an industry innovator. Trian convinced DuPont shareholders and executives that the company needed to “optimize stockholder value” rather than long-term growth. “This company (DuPont) is over 200 years old, and this guy who has nothing to do with the industry has basically got people on the board slashing R&D, just pumping money out of the company. And none of it is illegal,” argues William Lazonick, an economist at the University of Massachusetts-Lowell.

There is also activist investor’s shortsightedness as they only seek high, quick returns for a minimal investment. S&P Global Market Intelligence found that 40 percent of activist investors either reduce or completely relinquish their positions in the target company in just a quarter after making investments. According to Jeffrey Sonnenfeld, dean at the Yale School of Management, concern about the cost and bad press of proxy battles has motivated corporate boards to settle 45 percent of proxy battles in 2016, with many settlements involving invitations to activists to join the board. In 2001, only 17.5 percent of proxy battles were settled this way.

From a financial perspective, activists focus on monetary remuneration. Activist investors, Carl Ichan and David Einhorn, pressured Apple’s board and management to pay shareholders a substantial amount of the company’s cash resulting in a share buyback worth $40 billion and later had a $130 billion distribution in the form of stock dividends and another buyback. There was also Daniel Loeb through his hedge fund, Third Point, and its stake in Japanese robot maker, Fanuc. In 2015, Mr. Loeb urged Fanuc to make better use of its cash reserves. Fanuc decided to placate Mr. Loeb doubling its dividend payout ratio and establishing a new unit to communicate with shareholders. Finally, in 2015, McDonald’s was pressured by activist investors to make larger dividend payments to shareholders. McDonald’s relented and announced borrowing $10 billion to finance $30 billion in dividend payments to shareholders.

Debtholders are also affected by activist investor’s actions. According to a study conducted by Wan Wongsunwai of the Kellogg School and Jayanthi and Shyam Sunder of the University of Arizona, they concluded that activist investors both hurt and help debtholders, depending on the activists’ goals. Wongsunwai, et al., stated that, “Debtholders are sort of locked in. They make an investment [through a bond or loan] in a company, then typically remain hands-off. So, we can think of them as ‘bystanders’ who may benefit or suffer from activism.” They found that post-activism interest rates rose by 30 basis points, on average. They also concluded that there was a higher chance of debt defaults or payment delays, thereby creating more risk.

Serious Long-Term Consequences

While there are other negative consequences, one that can hurt all investors is that more publicly traded companies may decide to go private such as Dell. This saves them the aggravation of dealing with activist investors who have their own agenda, but hurt average investors who wish to diversify their holdings and achieve better long-term returns.

{kind=link}