By Arthur S. Guarino

China has an economy that is growing at a fast rate, but for various reasons it could suffer an economic collapse. Such a fall could affect the world’s economy and the numerous investors and companies having a stake in China.

China’s economy has been growing at a rate that is the envy of developed nations across the globe. In 2018, its economy grew at a rate of 6.6 percent with its gross domestic product (GDP) reaching $13.6 trillion. For the period from 1979 to 2010, China achieved an average annual GDP growth rate of 9.91 percent. For a nation that is relatively new in entering the global economic scene, this is very good. However, there are red flags that may signal China experiencing an economic collapse having global repercussions. This could mean global stock markets seeing serious declines, commercial banks experiencing heavy losses, and a deep recessionary period for many nations.

Reasons why an economic collapse could occur

The reasons why China could experience an economic collapse are quite varied but equally significant in their impact:

Trade war with the United States: The United States and China really need each other as trade partners. China is a key source of consumer goods coming into the United States whether it is iPhones by Apple or sneakers by Nike. China is a key market for American companies in services consisting of sectors such as insurance, banking, education, travel, and royalty payments. In 2017, the United States had a service trade surplus with China of $54.1 billion, while China has sent over $505.470 billion worth of goods to the United States. In 2017, the United States imported $78 billion worth of communications equipment, $24.5 billion in apparel, $14.1 billion in footwear, and $13.5 billion in motor vehicle parts.

China needs the United States: 21.6 percent of all goods imported into America in 2017 were from China, while Mexico was at 13.4 percent, Canada followed at 12.8 percent, with Japan trailing at 5.8 percent. If China does not have the United States as an export destination, the European Union, in its recent economic slump, will not be a successful substitute. While both nations need each other as trade partners, if the current trade war escalates because negotiations ultimately fail, then China could see a serious rise in unemployment and a continuing economic slump. The United States will also suffer serious consequences in a trade war as American consumers will pay higher prices for Chinese-made consumer goods. For example, American consumers were hit with $69 billion in extra costs due to tariffs the Trump Administration put on Chinese-made products in 2018 including steel and aluminum. An escalated trade war will hurt both nations, but perhaps China more so since it exports $3 worth of goods to America for every $1 in products imported from the United States.

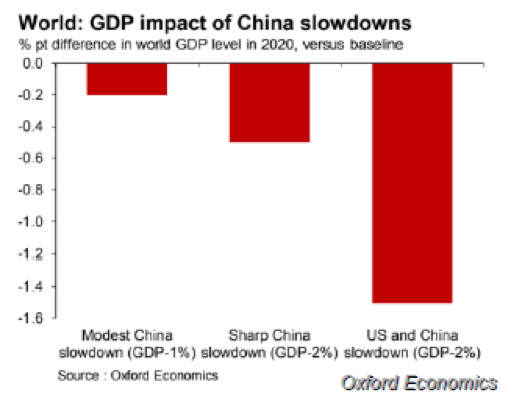

Weakening Chinese macroeconomy: A major worry facing Chinese President Xi Jinping is the slowing growth of the Chinese economy. After exhibiting double-digit growth for a number of years, in the last calendar quarter of 2018 China saw its economy grow at 6.4 percent as compared to the same time period for 2017. China also experienced just a 6.6 percent growth rate in 2018 which is the weakest rate of economic growth for the country since 1990. For an economy the size of China’s and with as many people as it has, going from a double-digit growth rate to 6.6 percent could spell economic collapse. China cannot afford a slowing economy in order to keep its people employed, businesses open, and its stock market growing. A trade war with the United States will not help Chinese industry since it must sell goods and products to its biggest customer without concerns about tariffs. Even if the global economy is showing signs of a slowdown, China’s economy is a clear indicator of the state of financial and economic growth.

Among the factors behind China’s weakening economy is a slow down in manufacturing, large investments by the central government and its provinces, lagging real estate sales, and a decrease in consumer spending. More specifically, regarding consumer spending this includes car sales that are down 19 percent in 2018 as compared to 2017. The ripple effect for China’s economy has been reduced production at its auto assembly plants which not only means reduced number of jobs, but ancillary products such as steel, aluminum, glass, and auto parts will also see a steep decline. China must make sure that businesses stay open and continue its cash flow levels so that they can pay off their loans and keep the state-run banks operating.What is also worrisome for China’s policymakers is that key items such as big-ticket spending has seen a dangerous decline. This can be seen in the decrease of fixed-asset investment in China in which it went from a rate of 34 percent in 2009 to 6 percent in 2018. Recently, Premier Li Keqiang, the second-highest ranking government official following President Xi, stated that China may be forced to reduce corporate taxes and use more deregulation as a way to stimulate the nation’s economy. Premier Li is echoing the government’s new policy of avoiding printing more money and increasing government spending programs. China’s policymakers are aware of the nation’s slowing economy and are making attempts to be proactive such as passage of a new foreign investment law by the National People’s Congress. Whether this and other actions will help China’s macroeconomy is still too early to tell.

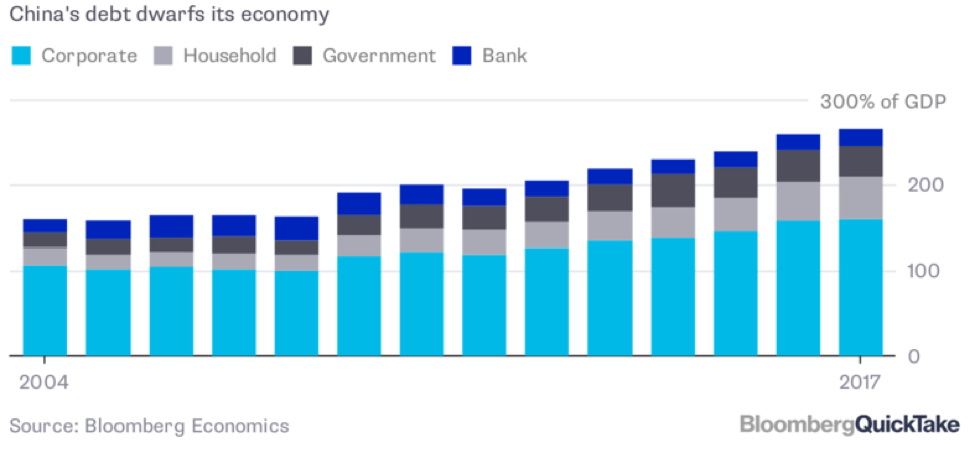

Too much debt: If there is one big concern that engulfs all of China it is the high amount of debt, both for banks and government. With China’s banks the problem is non-performing loans which have reached their highest amount in ten years ending in 2018. The Chinese government states that at the end of 2018 non-performing obligations were under 2 percent of total outstanding loans. This statistic has little credibility among financial analysts. For example, one analyst has estimated that $8.5 trillion in Chinese debt or 24 percent of total credit has gone bad. But looking at China’s whole economy, the nation’s current level of debt is estimated to exceed 250 percent of China’s GDP which exceeds the 150 percent from 2008. A bigger problem is that the amount of debt China acquires does not generate the increase in economic output that policymakers hoped for. The International Monetary Fund has reported that in 2008 1 trillion yuan of credit could generate 1 trillion yuan of economic output. But in 2017, it takes 3.5 trillion yuan of credit to generate 1 trillion yuan of economic output. The problem is that more financial capital will be needed to generate less economic output rather than the opposite result.

Adding to the problem of rising debt has been the increase of household debt in China. With China’s economy growing at a rapid pace, households are consuming more than ever before. But in many cases, this means more borrowing by households in order to afford the goods and services they consume. Currently, approximately 30 percent of China’s GDP consists of household debt with new loans by households making up almost 50 percent. These loans consist of residential mortgages, auto loans, credit cards, and other consumer-based debt obligations. As of mid-2018, outstanding mortgages made up 60 percent of all household debt. Mortgage lending has seen an average growth rate of 27 percent in the last three years, even though it has leveled off recently. Government authorities have imposed stricter lending requirements due to fears of a Chinese housing bubble. China’s credit card debt has risen dramatically and now makes up 14 percent of total household debt.

China also has debt problems with online peer-to-peer lending, microlending, consumer loans, and informal lending relationships. While China’s household debt-to-GDP ratio is approximately 50 percent, it is not as high as nations such as Australia (120 percent), the United Kingdom (80 percent), the United States (75 percent), or Hong Kong (70 percent), but given time and its growing economy China will reach their levels.Making matters worse is the amount of local and provincial government borrowing. State-owned banks make loans to local government entities in order “to fund risky land and property deals.” By 2015, local governments had taken out loans totaling approximately 18 trillion yuan for such types of deals. In 2015, the Chinese provinces were directed by the central government in issuing 2.6 trillion or $419 billion in bonds aimed at stabilizing the financial system. Because there was little to no demand for such financial instruments, China’s central government ordered state-owned banks to purchase the local bonds thus taking on more debt. There is also the situation involving off-balance-sheet (OBS) borrowings by local governments which some estimates have at 40 trillion yuan or $5.78 trillion. S&P Global Ratings likens this debt situation to “a debt iceberg with titanic credit risks.”

S&P also reported that including “hidden” local government debt, China’s ratio of government debt to GDP could reach 60 percent. At the end of 2018, China had outstanding government debt on its financial statements totaling 29.95 trillion yuan while OBS loans could possibly come to 30 to 40 trillion yuan. This includes bonds and local government financing vehicles (LGFVs) which have built a great deal of hidden debt. The bottom line is that China has a substantial amount of debt, official and unofficial, government, business, and household, that could create a significant economic and financial disaster if, and when, its house of cards tumbles.

What will happen next?

China’s economy has some key problems and its policymakers are aware of them. But leaders around the world are wondering how these problems will be handled or even addressed. China has a notorious reputation of claiming that everything is fine when actually it is not. Will China’s leaders become proactive or act too late?

{kind=link}